Breaking the link between debt and vulnerability

Our new briefing looks at the financial circumstances of our clients with vulnerabilities. Debt can have a serious impact on anybody’s life, but for people who are in a vulnerable situation, such as physical or mental health problems, or a life event, it can be even more severe.

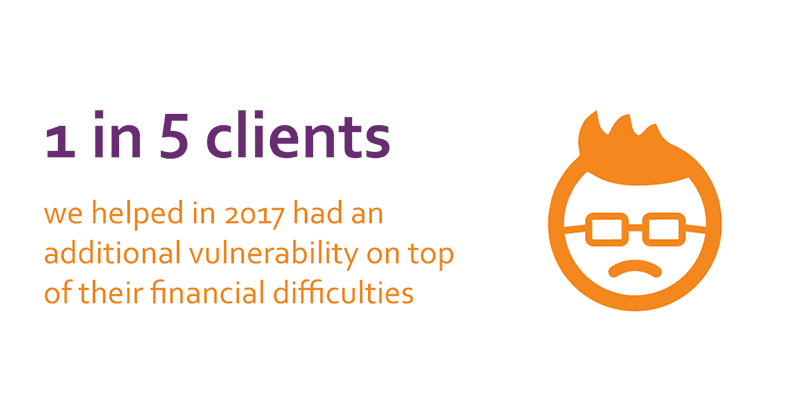

Our research found that in 2017, we supported almost 29,500 people who had an additional vulnerability on top of their financial difficulties. That’s the equivalent of one in five of the clients we helped in 2017.

At the sharp end of financial difficulties

Clients with vulnerabilities were more likely to be behind on their household bills and to have a negative budget, meaning they had less money coming in than they were spending on essentials. Our report also found that:

- Two in five clients with vulnerabilities said the main reason for them falling into debt was illness

- Almost half (45%) of our vulnerable clients had a negative budget

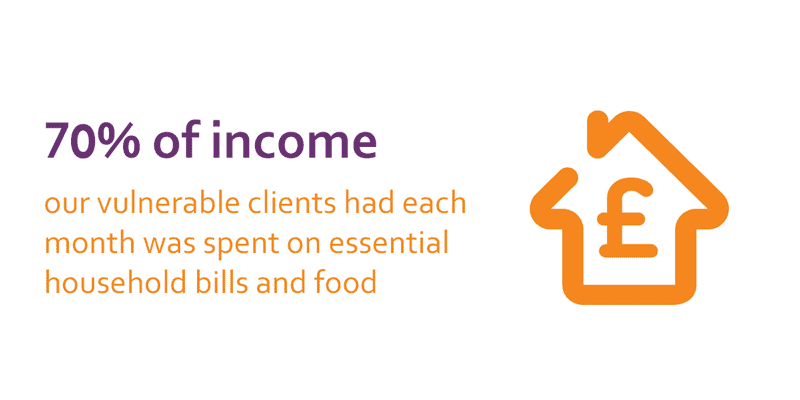

- Clients with vulnerabilities spent, on average, 70% of their monthly income on food and essential household bills like energy, rent, council tax and water

- 57% of vulnerable clients were behind on a household bill, compared to 40% of all clients

The high incidence of arrears on household bills and the stretched nature of people’s budgets all suggest that many vulnerable people are finding it hard to just get by on a day-to-day basis.

What should be done?

The challenge for us all – policymakers, financial services firms, utilities providers, debt collection and enforcement agencies and support organisations – is to make it so that people with a vulnerability get the support and adaptations they need to ensure they're at no greater risk of financial harm.

And, to reduce the negative impacts of problem debt so that it doesn’t affect people’s health and wellbeing. This is a huge challenge but one that should be at the top of policymakers’ agenda.

Download the report now to see our full research and recommendations.

Download now