Becoming a nation of savers

Our discussion paper builds on our earlier work to show, via new research, which families in the UK are least likely to have saved enough for a rainy day and offer options for how the pension auto-enrolment scheme could be adapted to deliver £1,000 savings for these families and others.

We also call on financial services firms to consider products to enable low-to-moderate income families to save, and suggest how the welfare system could be evolved to include a savings element.

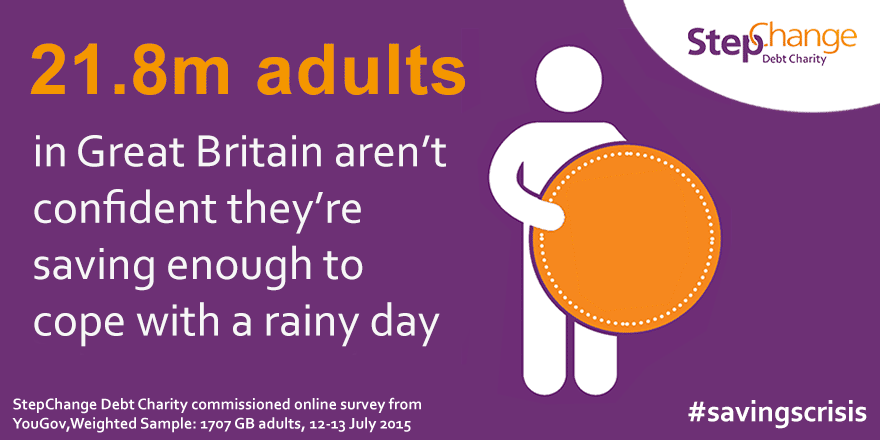

The savings crisis in the UK

Our latest research research shows that:

- People on low-to-moderate incomes, people in rented accommodation and people with younger children are least likely to have £1,000 in precautionary savings

- Economic influences such as low income and high outgoings are factors which prevents many families from saving

- Behavioural barriers such as bounded rationality, inertia and procrastination also prevent saving

The policy challenge is to get families saving by helping them overcome the economic and behavioural barriers which are currently preventing them from saving.

Our proposal

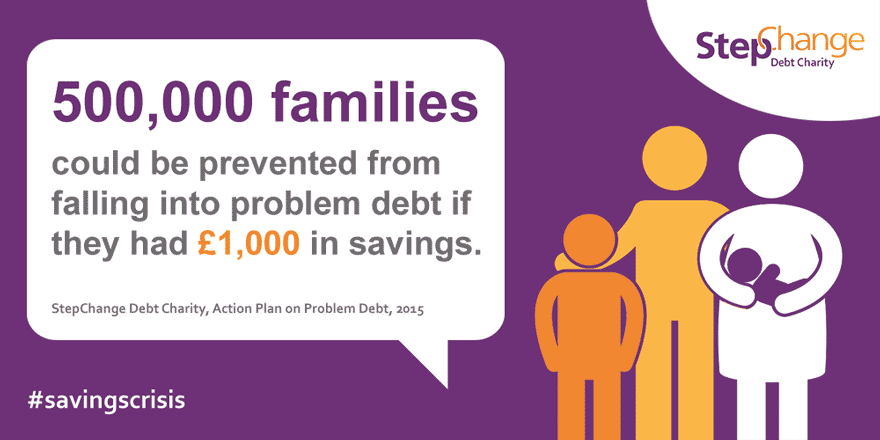

We want to see an improvement in financial resilience and a reduction in the level of problem debt in Britain. That's why we believe all families should have a minimum of £1,000 saved to help them cope during a 'rainy day'.

Incentives such as auto-enrolment, matched funding and prize-links have been used successfully in the UK and other countries to get families saving. We must use these incentives again to solve the savings crisis.

Our recommendations

- The government should set a target for all families in the UK to have at least £1,000 in accessible cash savings.

- The government should work with employers, pension providers and banks to allow struggling savers to build a rainy day saving buffer via the pensions auto-enrolment system. There are features of the model which would benefit from piloting, to test the effectiveness of different combinations of incentives

- Banks should explore, develop and ultimately pilot savings accounts which allow families to access preferential savings rates and offers even if they can only open accounts with a small deposit and only pay in small amounts on an intermittent basis subsequently.

- Financial services providers should explore the use of prize-linked savings accounts which appeal to lower-income consumers.

- Government should build a saving element into the welfare system via income thresholds and work allowances in Universal Credit and tax credits.

- Government should expand current trials of credit union accounts for pupils linked to financial education to secondary schools.

- Enhance the current proposal to include a savings element in the budgets of people receiving debt advice to resolve financial difficulties by:

a) formalising the saving from a provision in the individual’s budget to a deposit in an accessible savings vehicle;

b) ensuring creditors and essential services providers are fully engaged with the process;

c) the FCA explicitly acknowledging the benefits of saving in a client budget, as long as the consequences are fully explained to clients in terms of taking longer to pay down debt.

Download the discussion paper

There is much to do to overcome the savings crisis. But considering the benefit having a 'rainy day' fund brings to struggling families, it must be overcome. The UK already has many of the tools needed at its disposal to make the attempt a success. It should use them.

Download the discussion paper now for the full picture.

Download now